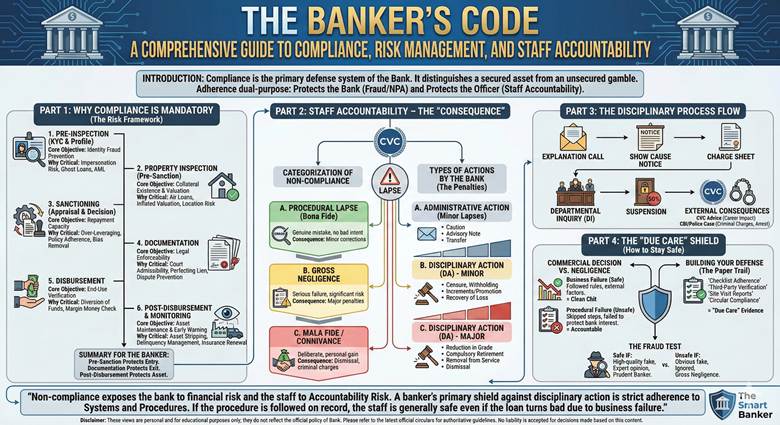

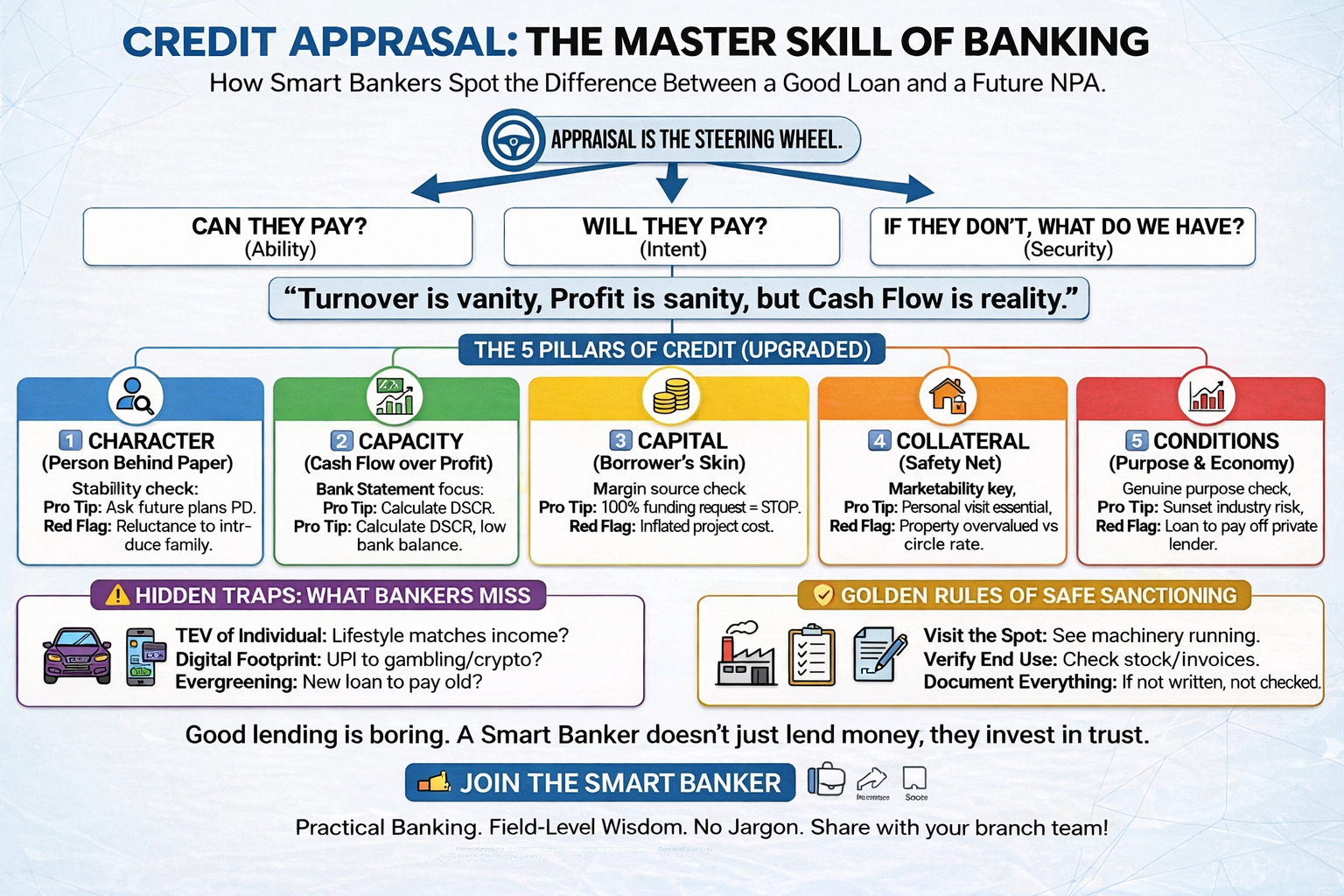

How Smart Bankers Spot the Difference Between a Good Loan and a Future NPA

Credit is the engine of banking, but Appraisal is the steering wheel.

A bank can survive low business for a year, but it cannot survive bad lending for a decade. That is why credit appraisal is not just a “process”—it is a defense mechanism.

This guide upgrades the standard appraisal process with practical, field-tested insights for the modern banker.

🔎 What is True Credit Appraisal?

It is not just ticking boxes on a checklist. It is a forensic investigation. You are answering three questions:

- Can they pay? (Ability)

- Will they pay? (Intent)

- If they don’t, what do we have? (Security)

🧩 The 5 Pillars of Credit (Upgraded)

1️⃣ Character (The Person Behind the Paper)

Documents can be manufactured; character cannot.

- The Check: Look at stability. Does the borrower shift residences or jobs frequently?

- The “Pro Tip”: During the Personal Discussion (PD), ask about their future plans. A genuine borrower speaks about growth; a risky borrower focuses only on getting the loan amount disbursed quickly.

- Red Flag: Reluctance to introduce family members or partners during the visit.

2️⃣ Capacity (Cash Flow over Profit)

- The Check: Don’t just look at the salary slip or P&L. Look at the Bank Statement.

- The “Pro Tip”: Calculate the DSCR (Debt Service Coverage Ratio).

- Red Flag: High turnover but very low average bank balance.

3️⃣ Capital (Borrower’s Skin in the Game)

- The Check: What is the Margin money source?

- The “Pro Tip”: If the borrower asks for 100% funding, STOP.

4️⃣ Collateral (The Safety Net)

- The Check: Marketability is key.

- The “Pro Tip”: Always visit the property personally.

- Red Flag: Property valued significantly higher than the market rate.

5️⃣ Conditions (The Purpose & Economy)

- The Check: Is the loan for genuine expansion?

- The “Pro Tip”: Check the industry trend.

⚠️ The Hidden Traps: What Bankers Often Miss

🕵️ The “TEV” of the Individual

- Lifestyle Check: Does lifestyle match declared income?

📱 The Digital Footprint

- Check UPI transactions to gambling or speculative apps.

- Frequent insufficient fund charges are a warning sign.

🔄 The “Evergreening” Attempt

- Watch borrowers using OD to service term loans.

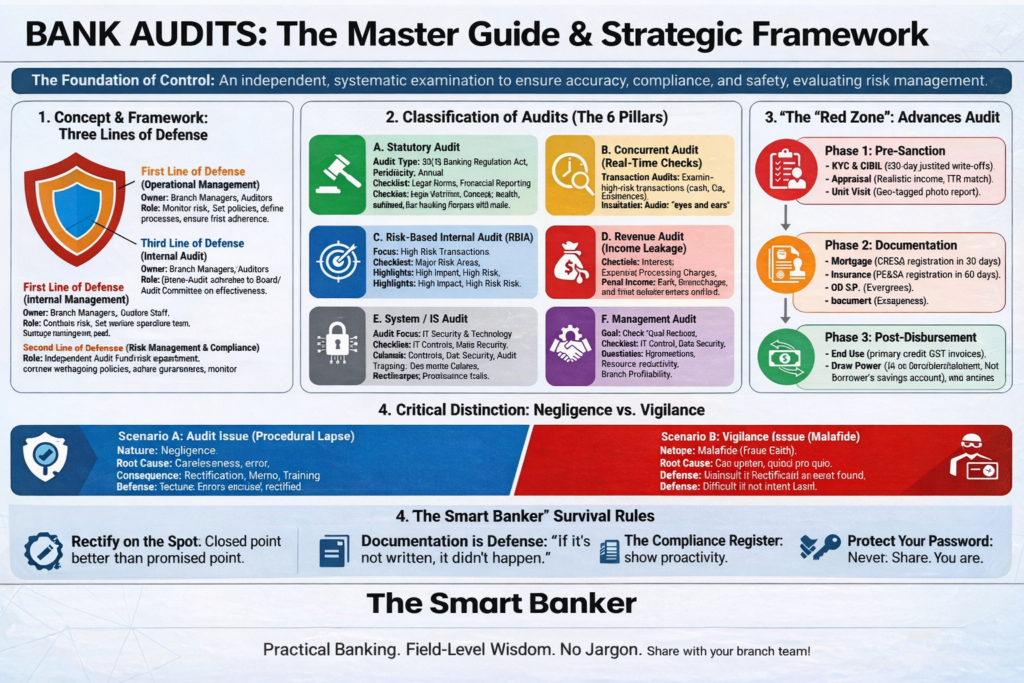

🛡️ The Golden Rules of “Safe Sanctioning”

- Visit the Spot.

- Verify End Use.

- Document Everything.

🌱 Conclusion

Good lending is boring.

It involves asking tough questions, visiting hot sites, and verifying dull documents. But this “boring” work builds a sleep-easy portfolio.

A Smart Banker doesn’t just lend money; they invest in trust.

Practical Banking. Field-Level Wisdom. No Jargon.

Share this with your branch team to stop the next NPA before it starts!

#CreditAnalysis #Underwriting #AssetQuality #LoanOfficer #CreditManager #BranchManager #SMEBanking #MSMELoans #TheSmartBanker #SmartBanking #BankingTips #FieldBanking