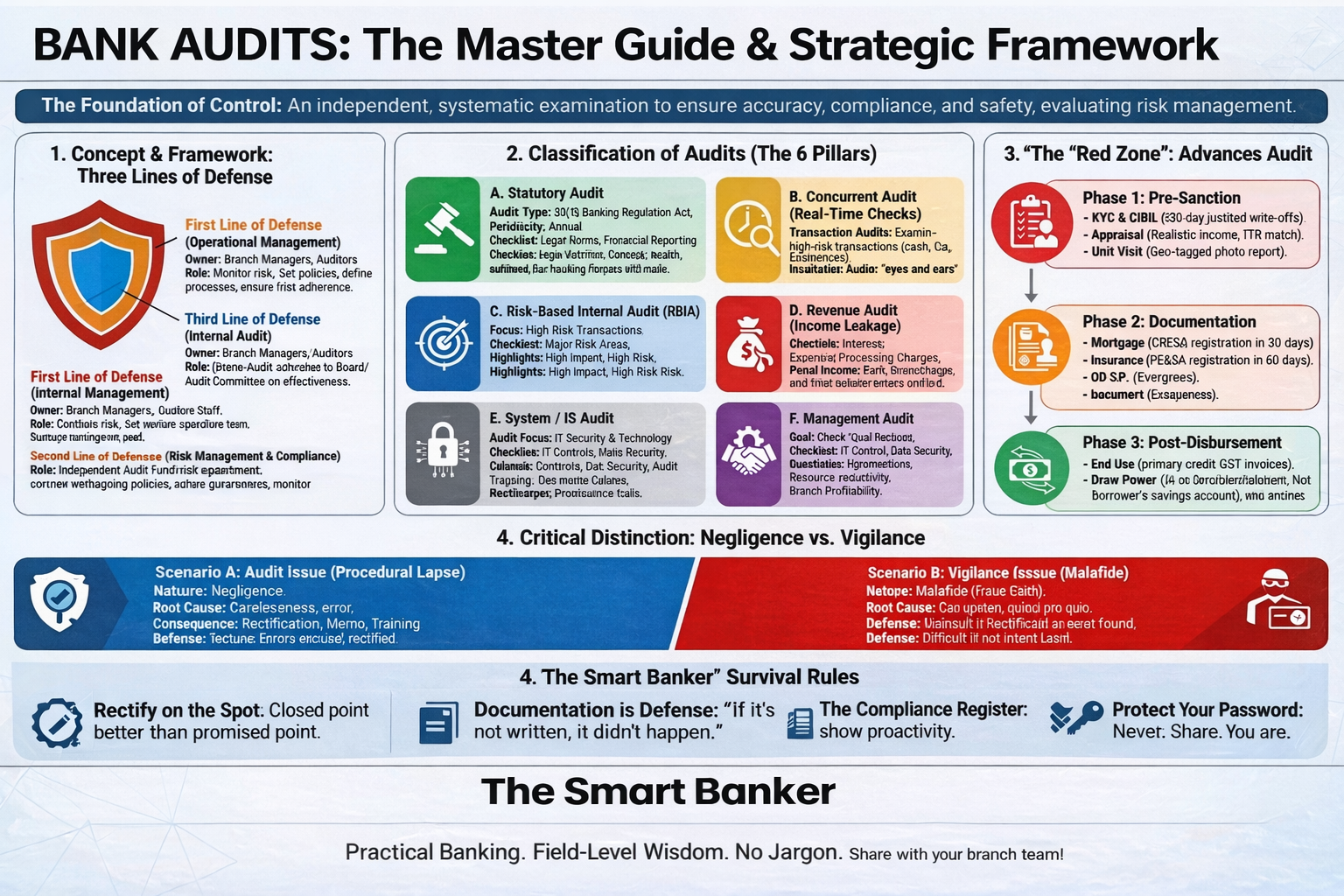

🔍 1. Concept & Framework: The Foundation of Control

Definition

An audit is not merely a “checking” mechanism; it is an independent, systematic examination of financial and operational performance. Its goal is to ensure accuracy, compliance, and safety. For senior management, the audit is a tool to evaluate the effectiveness of risk management, control, and governance processes.

The “Three Lines of Defense” Model

It is crucial for a Branch Head or Zonall Manager to understand exactly who owns the risk.

- First Line of Defense: Operational Management (Branch)

- Owner: Branch Managers, Credit Officers, Frontline Staff.

- Role: You own and manage the risk.

- Second Line of Defense: Risk Management & Compliance

- Owner: FGMO/ZO/HO Specialized Departments.

- Role: They monitor the risk.

- Third Line of Defense: Internal Audit

- Owner: Internal Inspectors/Auditors.

- Role: Provide independent assurance.

🧾 2. Classification of Audits (The 6 Pillars)

🟢 A. Statutory Audit

- Mandated under Banking Regulation Act, 1949.

- Key Deliverable: LFAR.

- Critical Output: MOC (Memorandum of Changes).

- Impact: Reclassification triggers Provisioning and affects Net Profit.

🟡 B. Concurrent Audit (Real-Time Checks)

- Concept: Examination as the transaction happens.

- Acts as an Early Warning System.

- Auditor liable if negligence is evident.

🔵 C. Risk-Based Internal Audit (RBIA)

- Focus on System/Process Auditing.

- Branches graded Low / Medium / High / Very High Risk.

- High Risk rating impacts performance scorecard.

🔴 D. Revenue Audit (Income Leakage)

- Detect unrecovered charges.

- Processing Charges.

- Penal Interest.

- Forex Margins.

- Locker Rent & GST.

💻 E. System / IS Audit

- Focus on CIA Triad: Confidentiality, Integrity, Availability.

- Password hygiene.

- Access rights & segregation of duties.

- Audit trail monitoring.

👔 F. Management Audit

- Focus on strategic decisions.

- Organizational efficiency.

- HR effectiveness.

- Product profitability.

📂 3. The “Red Zone”: Advances Audit

Phase 1: Pre-Sanction

- KYC & CIBIL validation.

- Income assessment realism.

- Geo-tagged Pre-Sanction Visit Report.

Phase 2: Documentation

- CERSAI registration within 30 days.

- Limitation validity (3 years).

- Insurance with Bank Clause.

Phase 3: Post-Disbursement

- End-use proof.

- Direct payment to Supplier/Builder.

⚖️ 4. Critical Distinction: Negligence vs. Vigilance

Scenario A: Audit Issue (Procedural Lapse)

- Nature: Negligence.

- Example: Insurance renewal missed.

- Consequence: Rectification or memo.

Scenario B: Vigilance Issue (Malafide)

- Nature: Malafide intent.

- Example: Bribe-based sanction.

- Consequence: Suspension / Dismissal / CBI Case.

🛡️ 5. “The Smart Banker” Survival Rules

- Rectify on the Spot.

- Documentation is Defense.

- Maintain Compliance Register.

- Protect Your Password.

Strong controls build strong careers.

Audit is not fear — it is protection.

Audit is not fear — it is protection.