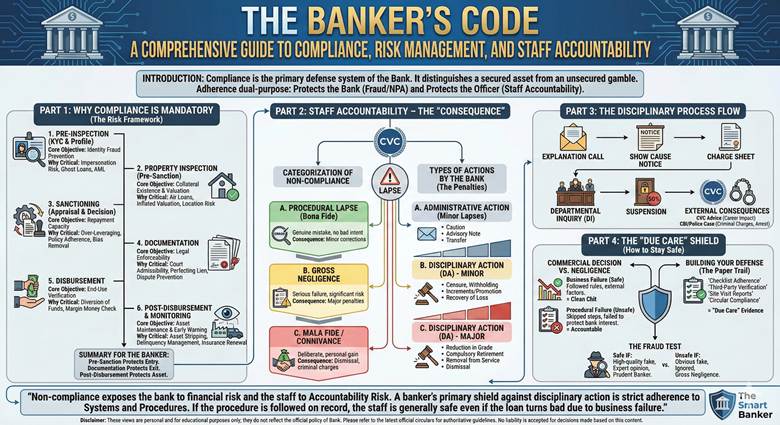

Introduction

In the high-stakes world of banking, “Compliance” is often misunderstood as mere paperwork or red tape. In reality, it is the primary defense system of the Bank. It distinguishes a secured asset from an unsecured gamble.

For a banker, adherence to Systems and Procedures is dual-purpose:

- It protects the Bank from financial loss (Fraud/NPA).

- It protects the Officer from administrative punishment (Staff Accountability).

This guide provides a detailed breakdown of why compliance is mandatory at every stage of the loan lifecycle and what happens when those protocols are breached.

Part 1: Why Compliance is Mandatory (The Risk Framework)

Every checklist point in a circular exists because a fraud or default has occurred in the past due to a specific loophole. Strict compliance is the only way to mitigate these risks.

1. Pre-Inspection (KYC & Profile Verification)

- The Core Objective: Identity Fraud Prevention.

- Why Compliance is Critical:

- Impersonation Risk: Without direct interaction and strict KYC, the bank risks lending to a non-existent person or an imposter using stolen documents.

- “Ghost Loans”: If the applicant is fake, the money is lost the moment it is disbursed. Since no genuine person exists, there is no one to recover the money from.

- AML (Anti-Money Laundering): Compliance ensures the bank is not being used as a conduit to channel illegal funds or finance terrorism.

2. Property Inspection (Pre-Sanction)

- The Core Objective: Collateral Existence & Valuation Accuracy.

- Why Compliance is Critical:

- “Air Loans”: Compliance prevents lending against properties that do not exist or are already mortgaged to another lender (Multiple Financing).

- Inflated Valuation: Borrowers often collude with valuers to artificially inflate the property price to secure a higher loan eligibility. Independent inspection is the only way to verify if the property is actually worth the loan amount.

- Location Risk: Inspections reveal if a property is in a negative zone.

3. Sanctioning (Appraisal & Decision)

- The Core Objective: Assessment of Repayment Capacity.

- Why Compliance is Critical:

- Over-Leveraging through ignoring NTHP/LTV leads to default.

- Policy adherence ensures risk alignment.

- Standardized norms prevent favored lending.

4. Documentation

- The Core Objective: Legal Enforceability.

- Court admissibility in DRT/SARFAESI.

- Perfecting the lien legally.

- Dispute prevention.

5. Disbursement

- The Core Objective: End-Use Verification.

- Diversion of funds prevention.

- Margin money verification.

6. Post-Disbursement & Monitoring

- The Core Objective: Asset Maintenance & Early Warning.

- Asset stripping prevention.

- Early delinquency detection.

- Insurance renewal monitoring.

Documentation Compliance protects the Exit (Recovery rights).

Post-Disbursement Compliance protects the Asset (The security itself).

Part 2: Staff Accountability – The “Consequence”

When compliance is ignored, it ceases to be a simple error—it becomes a “Lapse.” If a loan turns into a Non-Performing Asset (NPA) or a Fraud is detected, the Bank initiates a Staff Accountability Study.

Summary

“Non-compliance exposes the bank to financial risk and the staff to Accountability Risk. A banker’s primary shield against disciplinary action is strict adherence to Systems and Procedures. If the procedure (Checking, verifying, inspecting) is followed on record, the staff is generally safe even if the loan turns bad due to business failure.”